Highlights from our 1H 2026 Market Outlook

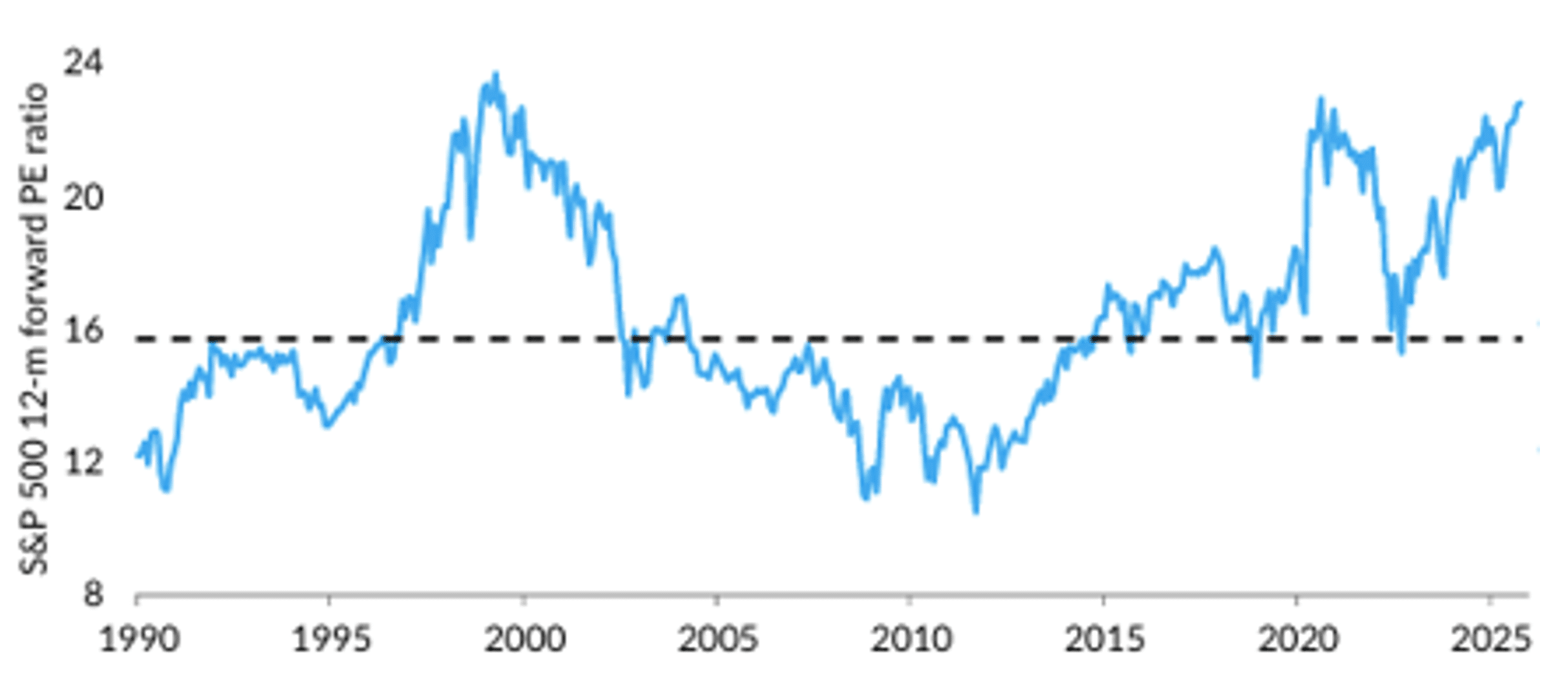

- US markets remain expensive as their forward P/E ratio nears record highs of 23x, well above a high MSCI Global equity forward P/E of 19.2x. We continue to recommend an underweight position in the US and especially in tech. shares.

- SA Inc. equities are extremely cheap and offer a generational buying opportunity.

- The political landscape remains precarious with municipal elections looming and Ramaphosa’s successor pivotal to our future.

- A case for a higher gold price can be made, but we recommend a smaller portfolio allocation as risks are increasing.

- The SA economy enters 2026 with some strong tailwinds, which could provide a growth surprise.

- We’ve been positive on the Rand, but recently it has strengthened too quickly against a weak Dollar: we expect it to stabilise around 17 to 17.50 in the nearer term, given the current political risks and anaemic economic outlook.

Global investment markets enter 2026 at record highs, which calls for a degree of caution when forecasting the outlook for the year.

The standout in 2025 was the US market significantly underperforming global markets and the SA market (JSE All Share Index -ALSI) significantly outperforming. The US was up 18%, MSCI Global Index (excl. US) up 32% and the JSE ALSI was up 42%.

Our market views ending 2024 were firmly to be underweight the US and overweight Europe, Emerging Markets and South Africa.

The JSE’s phenomenal rise in 2025 was mainly due to precious metals (Gold and Platinuim) up 200% and Naspers up 35%. The rest of the market was reasonably flat as foreign investors continued to disinvest as local economic growth disappointed at only 1.3%.

In 2025, global investment markets were often kept guessing due to an unpredictable Trump, which fuelled constant volatility. Despite this, global markets pushed on to record highs despite falling 10% in April, due to Trump’s tariff announcement.

The main investor themes in 2025 were: Trump, US tariffs, AI, Gold, inflation uncertainty, and an escalation of global conflicts.

2026 investment markets have kicked off on the up extending near record high valuations. The main themes are likely to be:

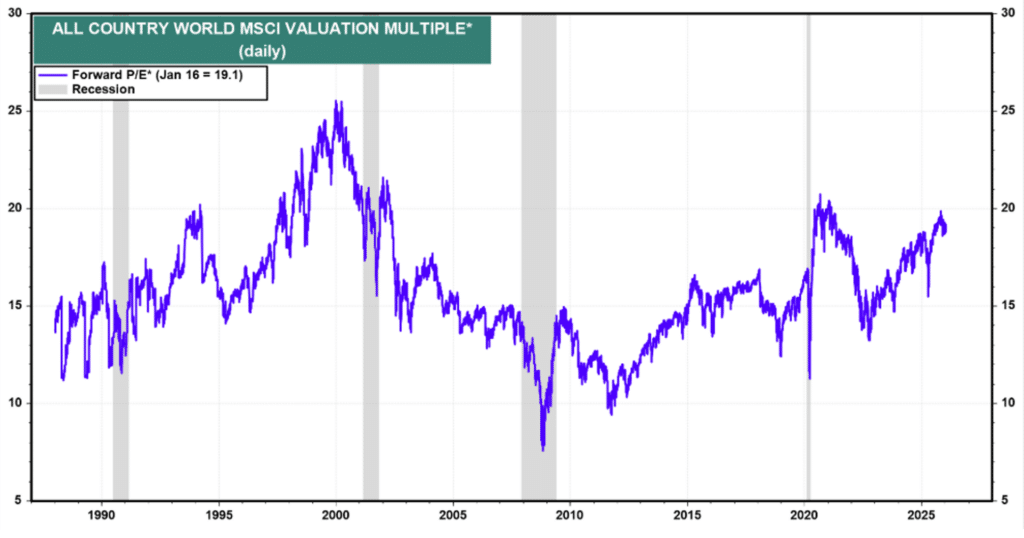

High global equity valuations

The global equity index forward P/E is 19.1x, which is well above its 30-year average of 14.8x. These high valuations are predominately driven by the US, which we believe is expensive on a forward P/E of 23x.

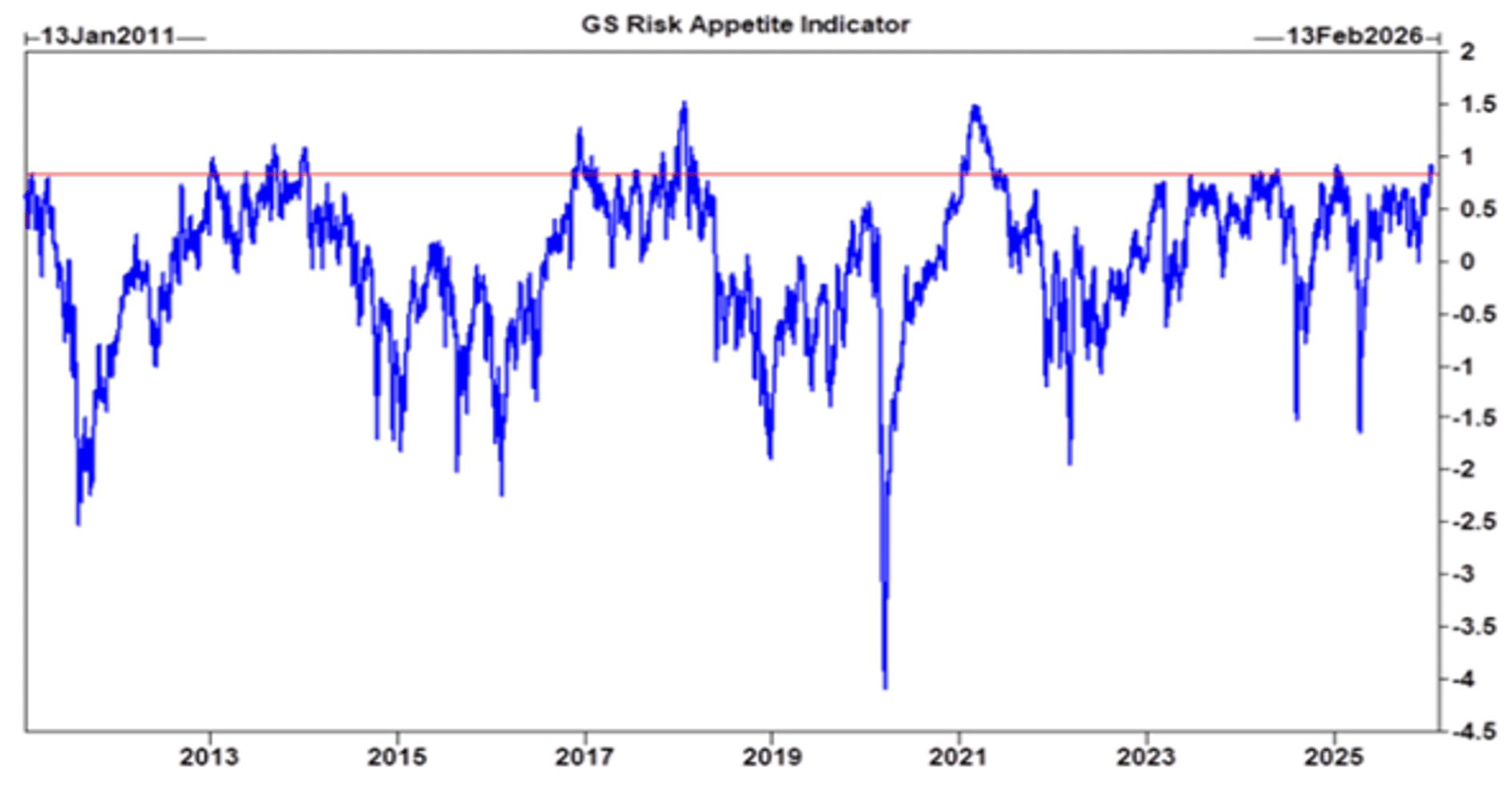

Although an AI bubble is widely discussed, there appears to be a general complacency in the markets, with risk appetite near all-time highs.

Goldman Sachs Risk Appetite Index

The US inflation outlook remains uncertain

US core inflation is currently 2.6%, above its target range of 2%, which restricts meaningful interest rate cuts. Currently the market is pricing in 50bps of cuts in 2026, but more cuts are needed to uphold economic growth.

Trump is under pressure for US growth to improve to support his political careers, and he continues to pressurise Federal Reserve Chairman Powell to lower rates. With Powell’s tenure ending in May, there is concern that a successor may prioritise lower interest rates to align with political pressure, potentially driving higher inflation and creating headwinds for markets.

Trump remains a market threat

There is a view that Trump will have less gravitas for investors in 2026 as markets have become less fearful of his threats. However, the current mid-term election polls for November show a poor outcome for Republicans (Trump) and point to them losing the House of Representatives to the Democrats, which could also lead to losing a majority in the Senate. This will significantly curtail Trumps’ power, of which he is very aware and could lead to him taking more radical action to regain popularity.

Where next for Gold?

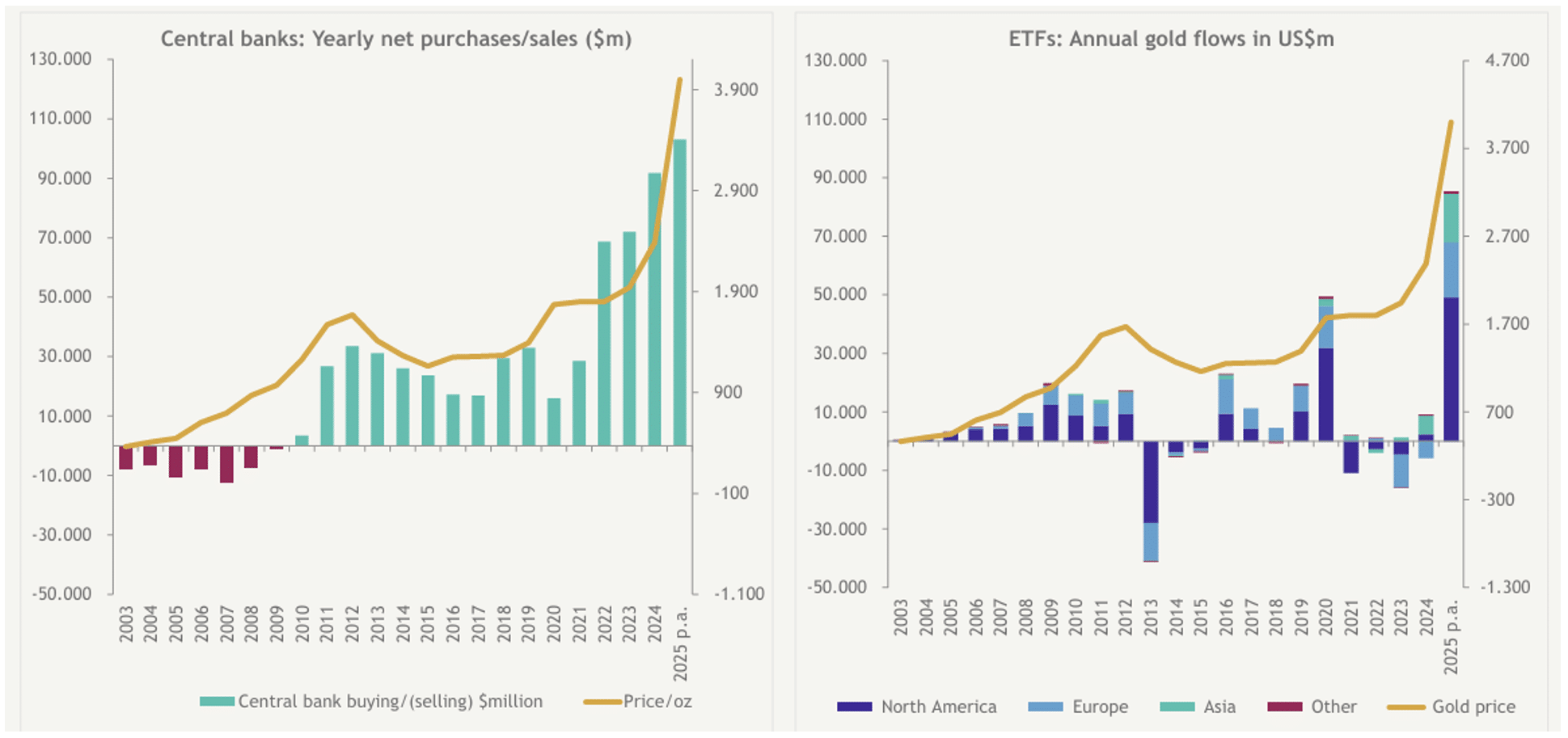

The gold price is at an all-time high.

Gold has always been notoriously difficult to predict resulting in most investors having low gold holdings in their portfolios.

The two major drivers of the gold price are low to negative real interest rates and economic fear. This spike in the gold price is driven by the fear that the world is too reliant on the US Dollar. Consequently, many countries, mostly in the East, have been diversifying their foreign reserves into gold.

Recent activity prompts the question, will central banks keep buying gold which will push the price up or does this spike lead to a collapse ? Trump has fuelled most of this fear and as long as he remains unrestrained, this fear is likely to remain. Certainly until the November mid-term elections.

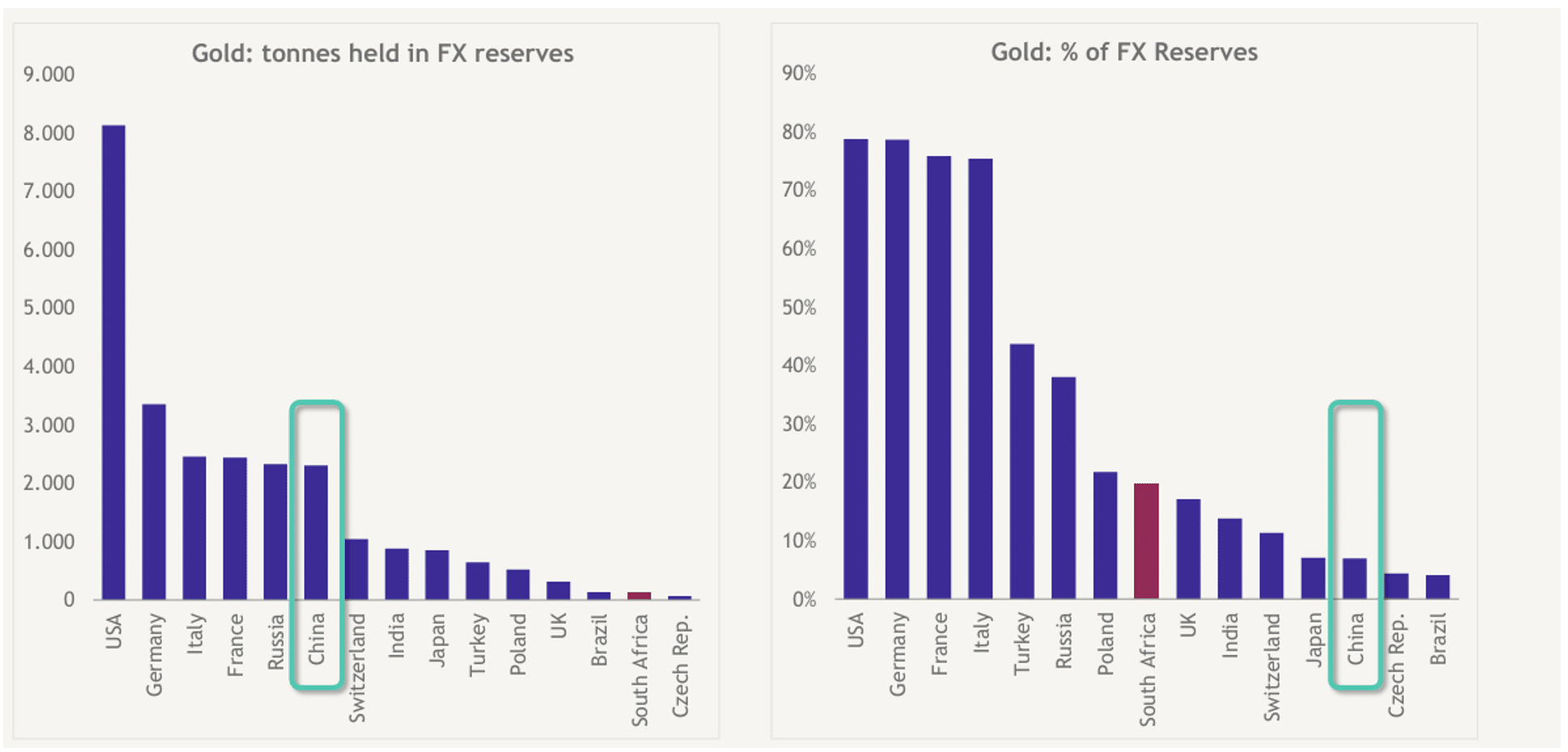

The charts below show gold as a percentage of country reserves with China standing out with a low percentage of reserves, which provides scope for further buying if the US fear escalates.

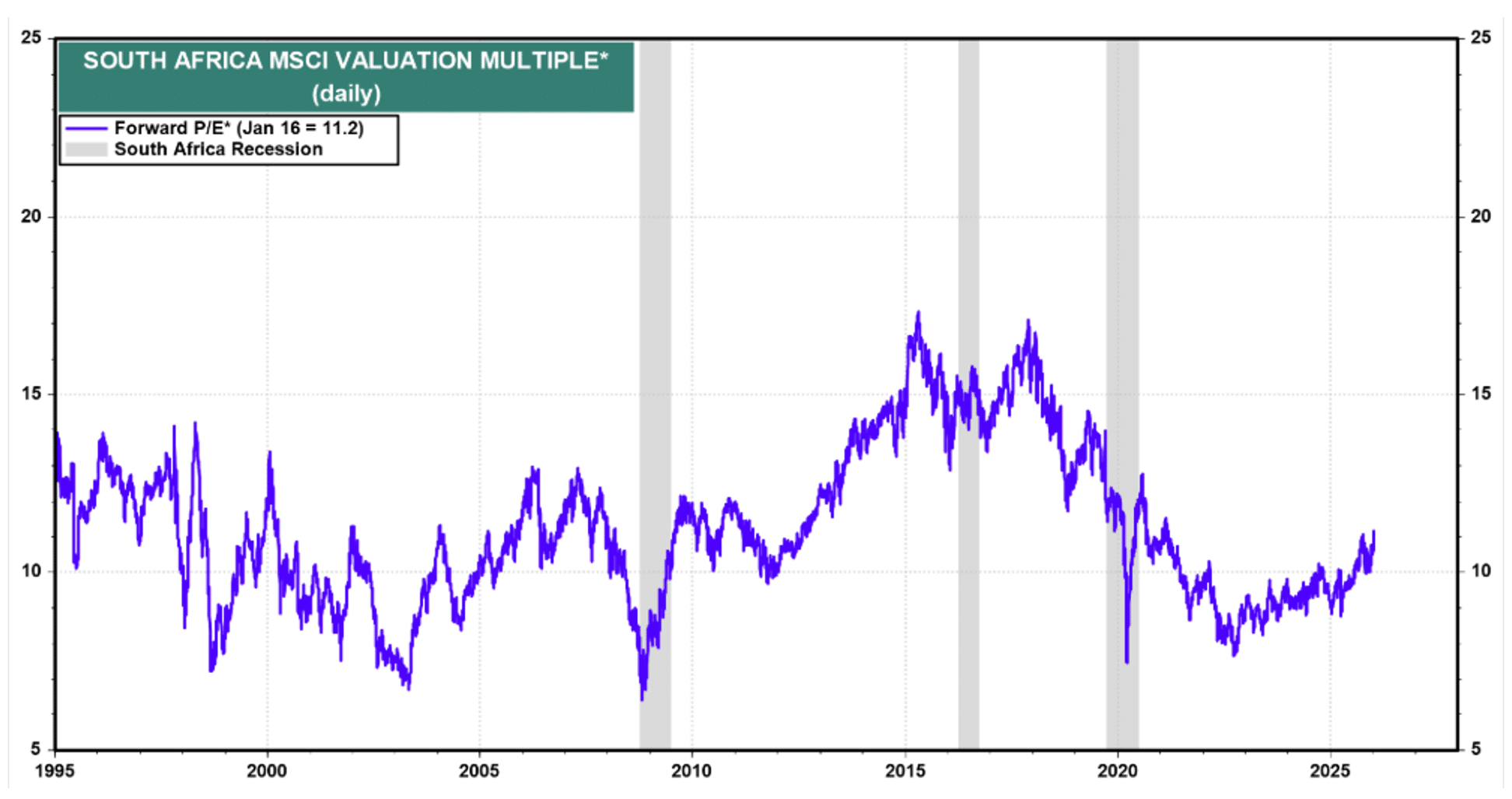

SA shares are cheap, but we need economic growth

Despite the recent strong rally in precious metal shares and Naspers, overall, SA shares are still cheap, trading at a forward P/E of 11.2x, well below its 30-year average of 13.5x.

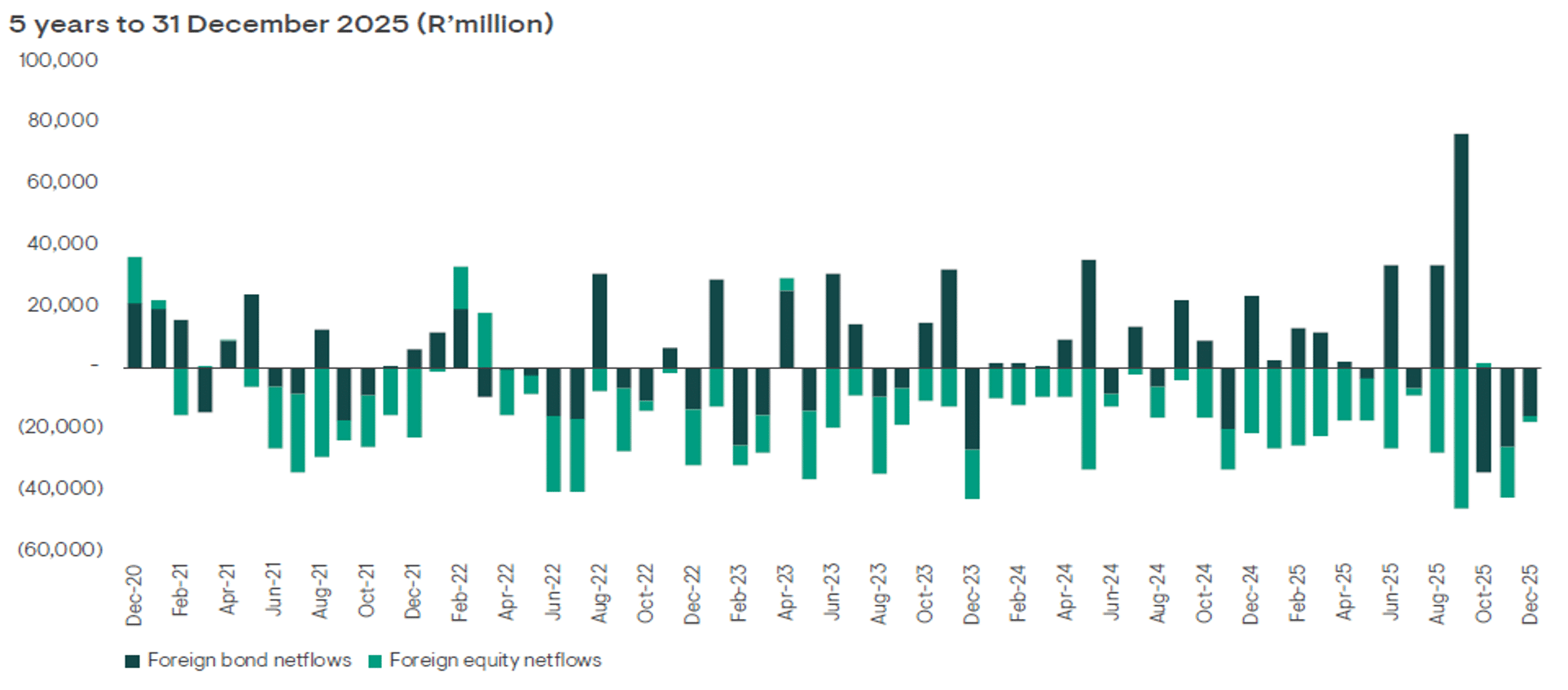

SA Inc. shares (companies that derive most of their revenues within South Africa, such as banks, retailers, property, and industrials) were mostly flat in 2025 as foreign investors continued to disinvest as economic growth remained weak. The conundrum, however, was that foreigners were buying our bonds as the risk of a government debt spiral eased, thanks to stronger debt-anchoring policies and higher tax receipts.

SA MSCI index forward P/E

However, to unlock meaningful value in SA Inc. shares, the South African economy needs to grow at a significantly higher rate—at least 3%. Until there are clear signs of stronger growth, much-needed foreign investment is unlikely to flow into our market.

Foreign selling of SA shares continued in 2025 with overall ownership staying below 30%, down from 40% in 2021.

Foreign netflows of SA bonds and equities

SA’s anaemic economic growth of 1.3% in 2025 and forecast at around 1.5% in 2026 and 2027 has the country going backwards as unemployment should continue to increase and government debt will rise. For growth to increase we need investment from local and foreign companies, and this will only take place with political stability and government reliability.

SA politics on a ”knife’s edge”

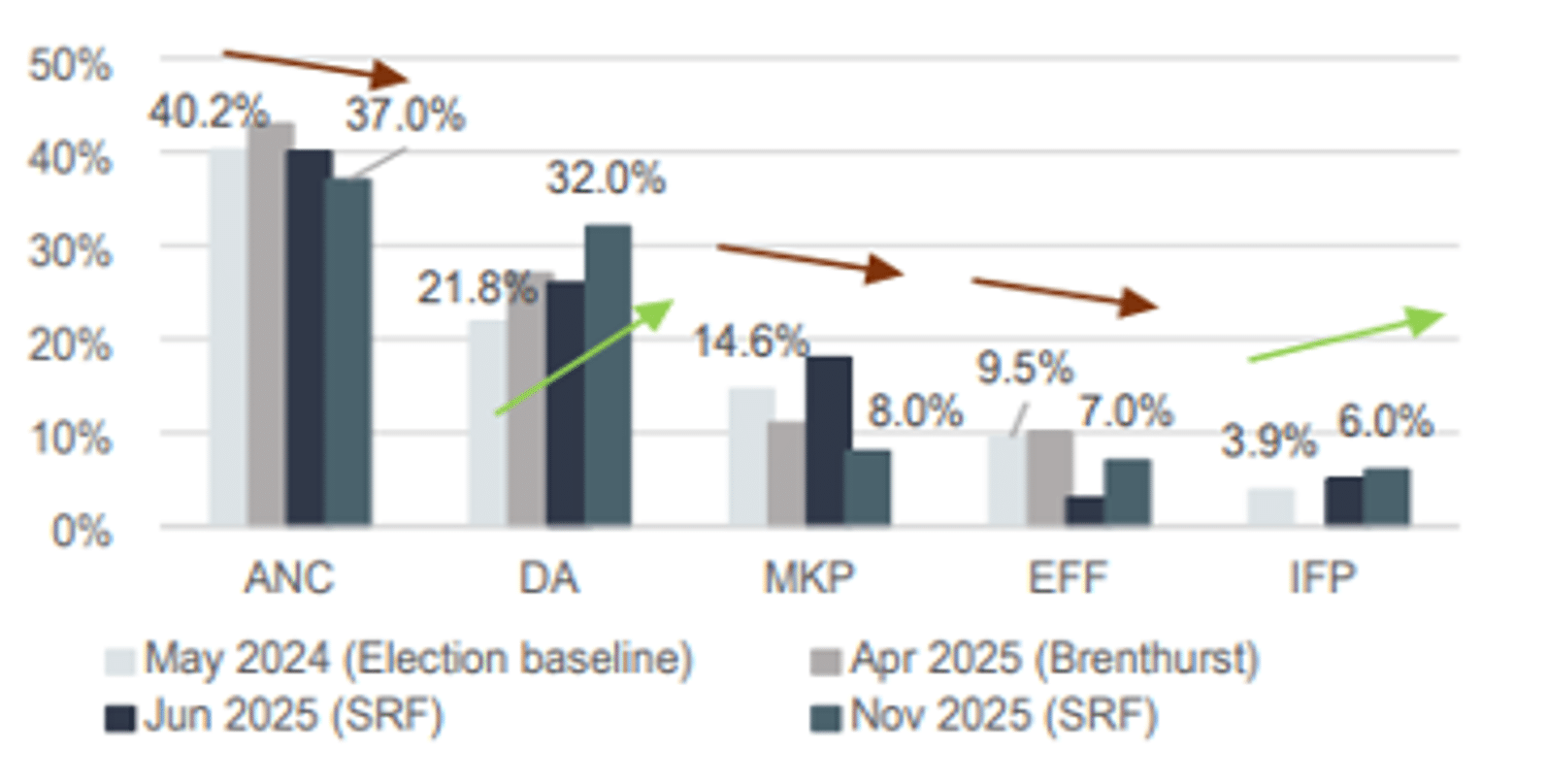

Municipal Elections could be the tipping point

The ANC’s support has slipped to 37% per the latest polling. Some analysts assert that this declining support is unlikely to stop without some major improvement in government delivery or changes in the ANC. The latter is more likely and does not bode well.

SA political polls

A most crucial indication of where we are headed will be the result in Johannesburg which hopefully will be the demise of the ANC’s leftist faction.

Who will succeed Ramaphosa?

This is the most frequently asked question by investment fund managers of political analysts, which is consistently met with: unsure/I don’t know.

In our opinion, this is the single most important issue in SA, because even with a less popular ANC, they carry enormous weight in who they will side with – DA, MK or EFF. This will have a major impact on the future of the country.

SA’s economy disappoints but there is real upside potential

Although forecasted economic growth of 1.3% in 2025 was disappointing there are many tailwinds taking us into 2026:

- Inflation is expected to remain steady in 2026 averaging 3.3% as per last year. This should lead to interest rates being cut 50 to 75 bps, which would be very positive for the economy.

- Major government infrastructure departments, Eskom, Transnet, Ports and Sanral, are all making significant improvements to their structures for service delivery.

- Global institutions have turned more positive on SA following Treasury’s reduced inflation target to 3%. In December, the IMF produced a positive report on SA.

- Moody’s kept our rating at Ba2 (stable), citing strong institutions, but persistent structural and debt challenges. S&P also raised our rating and maintained a positive outlook on the back of stronger growth and improved finances.

- We’ve been removed from the EU list of “high-risk third country jurisdictions”. This follows our removal in October from FATF’s (Financial Action Task Force) grey list.

- The House of Representatives in the US has extended SA’s participation in AGOA, which will next go to the Senate before final approval from Trump.

- Demand for platinum group metals is improving as electric vehicle market shares are slipping in Europe and the US. This is a structural positive for the mines and suppliers.

- The National Treasury’s efforts to slash wasteful government spending appears to be bearing fruit, with R6.7 billion worth of underperforming programmes set to be closed or scaled down immediately.

- SA wins include a R16bn World Bank loan to revive eight major cities, including Johannesburg, Cape Town, and Durban.

- Signs of infrastructure and building improving is real as construction companies’ order books swell.

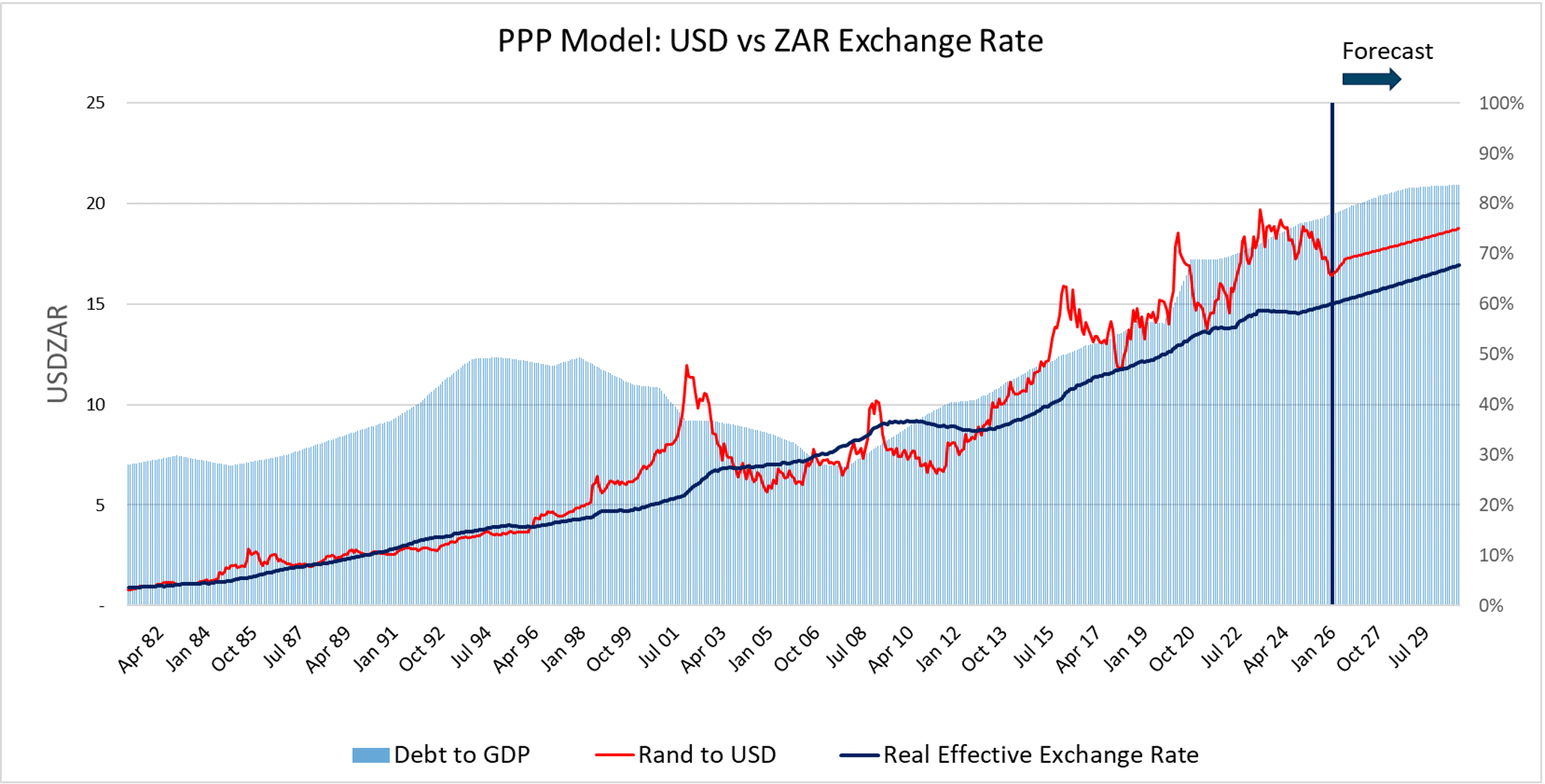

The Rand/Dollar is firm due to a weak US Dollar

We’ve been positive on the Rand, but recently it has strengthened too quickly despite the weak Dollar. We expect it stabilise around 17 to 17.5 in the nearer term, given the current political risks and anaemic economic outlook.

Over the last 12 months, the US Dollar Index (a basket of world currencies) has declined 10%. Consequently, the R/$ has strengthened by 13%, but the Rand has only strengthened 4% against the Pound and is flat against the Euro.

US Dollar basket of global currencies Index

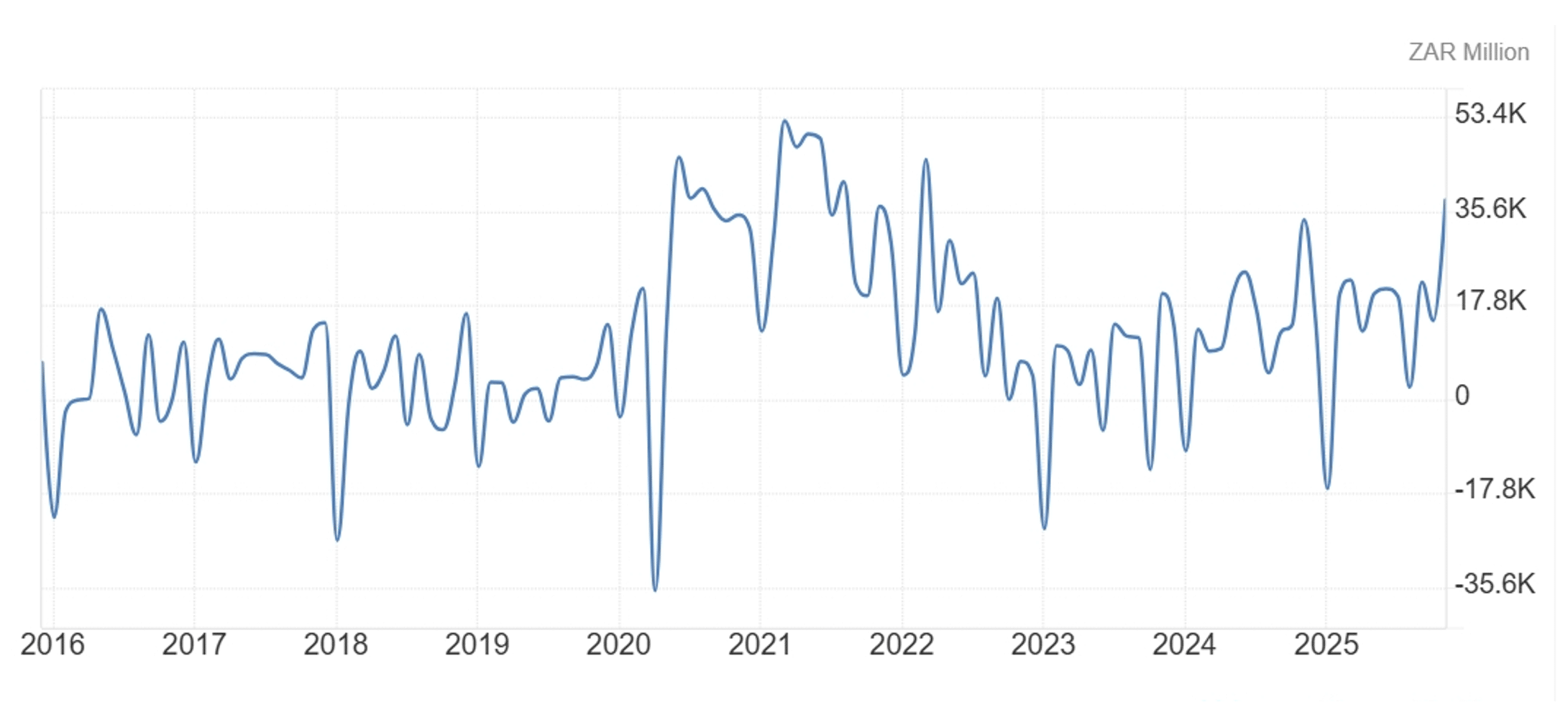

The Rand has been supported by a sharply improved trade balance, as exports of precious metals have surged while imports remain weak due to the soft South African economy, and the decline in oil prices has also provided a tailwind.

SA Trade Balance

Given the current political risks and economic outlook, we believe the Rand/Dollar rate should fundamentally be around 17.25. This reflects a purchasing power parity (PPP) of 15, plus a 15% judgemental risk adjustment premium. This premium is down from a previous implied 30% in 2024, primarily due to the improved government debt outlook from the new fiscal consolidation policy.

The Prosperity Fund continues to produce solid and steady returns

The fund produced a steady 13.3% return in 2025, which supports its solid 10-year track record of average compound growth of 10.4% p.a.

The fund prioritises capital preservation through conservative management. It is designed for investors seeking a balanced portfolio that includes local and international exposure and generates consistent investment returns. The fund reflects Investonline’s in-house market views, which we aim to replicate across different investment risk strategies for our clients.

Its unique investment management style primarily involves taking short-term tactical positions in asset classes that are irrationally priced, based on a combination of top-down and bottom-up fundamental research. To a lesser extent, longer-term strategic positions are incorporated when major market opportunities are identified.

Market Outlook

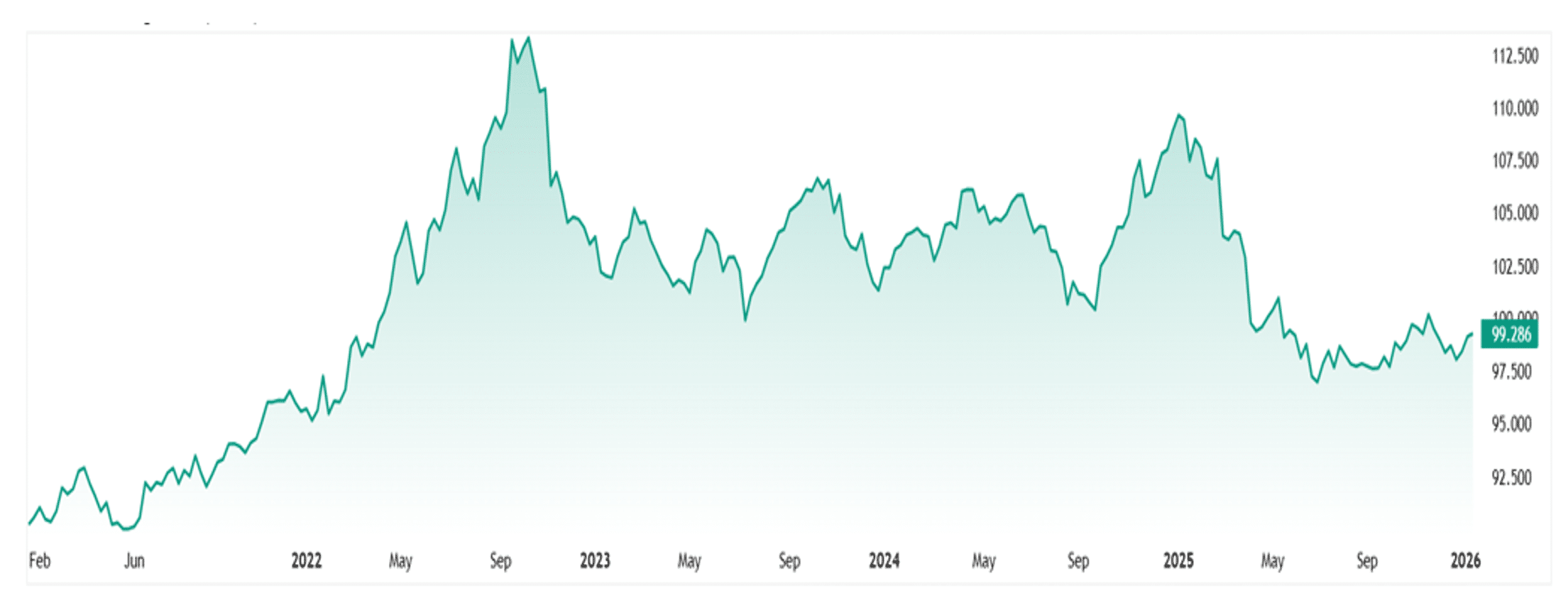

US markets remain expensive as its forward P/E ratio nears record highs of 23x, well above a high MSCI Global equity forward P/E of 19.2x. We continue to recommend an underweight position in the US and especially the overextended technology sector.

S&P 500 forward P/E ratio

With global market valuations high, we prefer active funds over passive funds. Passive funds are vulnerable to the market’s high concentration risk unwinding and active funds should be able to take advantage of the many value opportunities that still exist.

Potentially, low oil prices and firm commodity prices bode very well for SA. This promotes the SA Inc. investment theme which can be described as a “generational opportunity”.

Overall, we still prefer Emerging Markets and SA equites.

Review your Investment Strategy

With global investment valuations widening, it’s essential to ensure that your investment portfolio is properly balanced and aligned with your personal risk profile to achieve your financial goals. Regularly review your financial plan to ensure it remains up to date. It is crucial that the risk you take in your investment portfolio aligns with your financial plan, particularly as you approach or enter your retirement years.